Pump Up The Jam

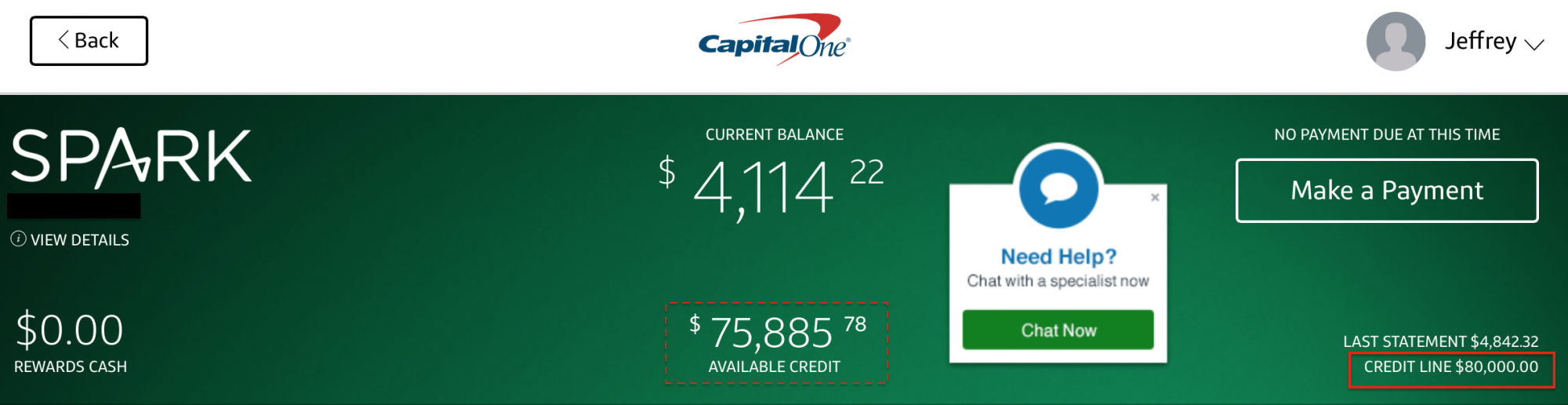

A few days ago I began the day as I usually do – paying bills. I have significant spending on my rewards cards every day, so I keep a spreadsheet with my outstanding obligations, balances and pay bills regularly. Compared to some heavy hitters in the rewards game, my credit lines are all pretty conservative, with none over $20,000. Some of that is done by design (some have been intentionally lowered), and some is done by the bank upon approval. That morning after logging in, my Capital One 2% Spark Cash for Business credit line jumped from $10,000 to $80,000, or a 700% change – overnight, without my prodding or approval.

Initially I thought something was wrong with Capital One’s site. Perhaps there was an electronic glitch that bumped up my credit line artificially? Then I thought maybe the bump was caused by last year’s spend on the card, and that Capital One was just adjusting my credit limit to be more in line with my monthly manufactured spending prowess. Then I reached out to a few heavy MSers who had similar issues.

“Close the card”, they said. It was like an echo chamber of feedback.

“Excuse me”? I replied back in shock.

Basically a massive credit limit increase is somehow tied to a spending review, which in turn puts eyes on the account. Long story short, when a dramatic credit limit like this occurs, the account is destined for a shutdown. When the looming shutdown really takes place wasn’t really important. Since the credit limit bump I had already put some MS spend on the card, so to me that was grounds for a more immediate shutdown. With that said, fear took hold, and the following morning I called Capital One, used my cash back via a statement credit, made a final payment over the phone for the remaining amount owed, and closed the account.

Lesson Learned

Looking back I think I may have created the eyes on account and credit limit increase from my own actions. About 3 weeks ago I applied for the Capital One Venture Miles card, which I hoped would replace my Barclay Arrival Plus that was closed last year. Bank points like Capital One and Barclays have been useful for some recent adventure trips including an African safari and great white shark cage diving in South Africa and Australia.

In preparation for the Venture Miles card application, I waited 5 months between app-o-ramas, applied for the Capital One card first, and was confident that I’d taken the necessary steps for an approval. To my surprise I was denied. The reasons for the denial were sent in a letter that I received a week later: too many recent inquiries, and balances on too many credit cards. Over a week later I decided to appeal the decision, hoping that someone in the credit department may arrive at a different conclusion.

That appeal didn’t go far, as I didn’t change anything on the original application. Apparently something needs to change (more income, additional informaiton) in order for the reconsideration to actually take place. But somewhere in that process, it may have opened up my account to having the wrong set of eyes on it. Once patterns emerged, which on this particular card were completely obvious, my account was flagged.

Summary

I’ll never know exactly what happened to get my account on the watch list. It’s probable that outside of MSing the card, my actions caused the credit limit to spike and get the shutdown wheel to start turning. In the end the Capital One card served as a great cash back resource for over a year. It did it’s job, and I was able to close the account before the bank shut me down. That turned out to kind of be a win-win proposition, but I am now down a major resource in my wallet. The good news is that a similar card is in the mail that should pick up the slack very nicely, albeit with a smaller credit limit.

Things are getting more precarious in the points world with shutdowns becoming more common as banks tighten their risk belts. Remember that your actions will have reactions, both good and bad.