An Old New Card

As I’m becoming more inspired by FIRE (financial independence retire early), I’m becoming more and more of a fan of cash rewards vs. points. Fortunately there’s still plenty of opportunity to earn rewards with high end value and often those rewards will greatly outperform the returns from cash. However, as I’m saving money at higher rates (and cutting expenses), cash rewards are becoming more compelling for me. A few weeks ago I cashed out a million Ultimate Rewards for $10,000 in cash. That cash-out was at a pretty lean 1% rate, but I did list reasons for that decision in my post. I’ve done similar things in larger and smaller scales too, but have done so without writing about it.

Cash back reward structures vary. Citibank has a Double Cash product that pays 2% total, but 1% with each charge, and 1% after payment is received. Penfed allows for statement credit or a transfer of funds into a linked checking account, while the Fidelity Rewards Visa Signature also allows users to redeem cash back into investment accounts. Beyond those reward structures though, are the intricacies in how readily rewards can be accumulated. The knowledge of each bank and their respective rewards program is more significant than how rewards are distributed. Play within the established (and often non-established) lines for each bank and you can do very well, but step outside those lines, and you’ll have issues, some of which will lead to a problems like shutdowns.

App-O-Tite

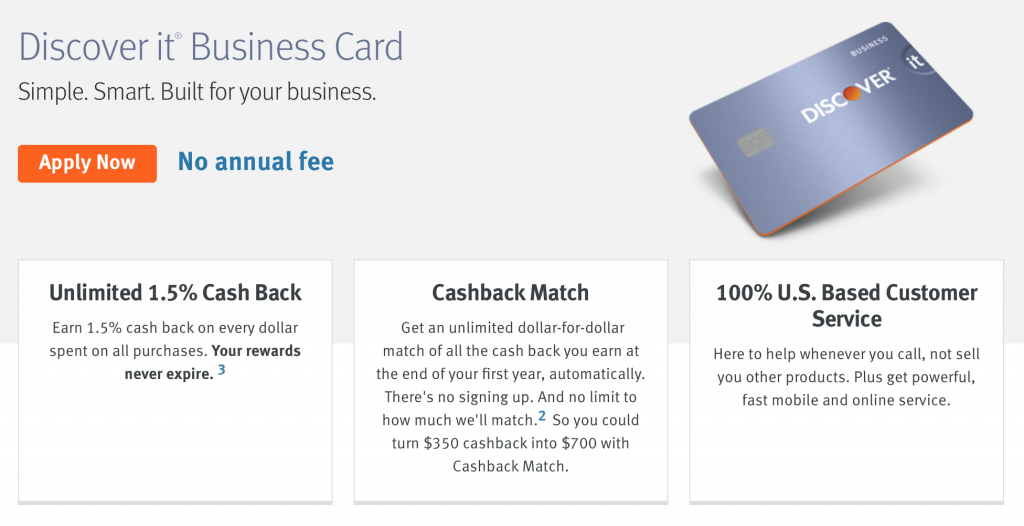

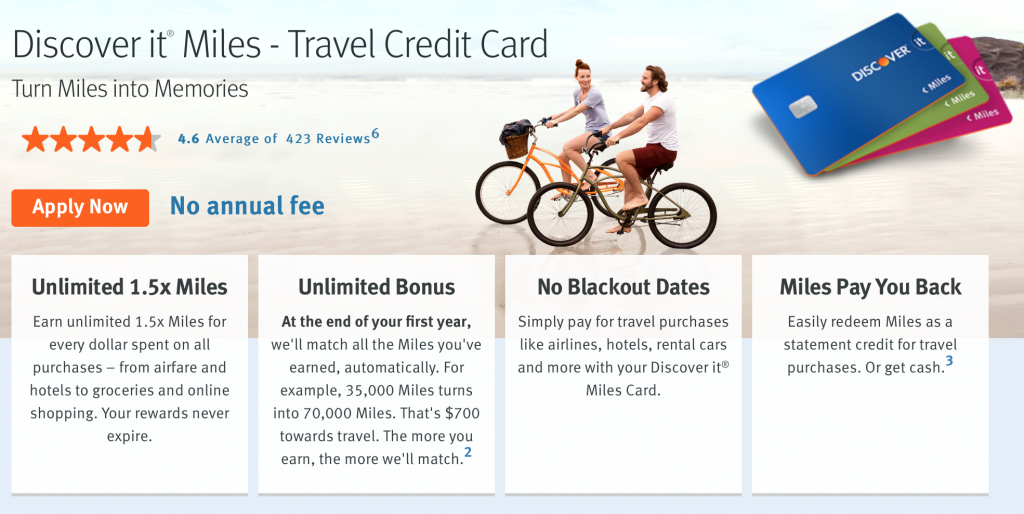

Ok enough babble. I’m applying for a new set of rewards cards soon, and thanks to my recent Bank of America and Citibank shutdowns, I’m filling some holes in my portfolio and exploring new paths as well. One card that caught my eye, that I’d hadn’t heard or read about, is the Discover It Business card. It’s not some super secret card, as I’d imagine it’s been out for the same timeframe as the personal Discover It Miles product, but for whatever reason has fallen under the blogosphere’s radar. I assume the card has fallen under the radar because 1) people, including points bloggers, didn’t know it existed, 2) if they did, perhaps Discover doesn’t pay as well as other banks do for affiliate links. In the end, I guess the reason why there’s no chatter about it doesn’t matter much, but the card it solid, and I’m listing it here in case someone had an interest in a possible spot for it in their wallet.

1.5x points earned in year 1 are matched to make the business card a true 3% points or cash back option

Other than the superficial design of the card, the rewards layout is very similar to the personal Discover It Miles card. The “No Blackout Dates” language differs with the two products, but since that’s not my path with this product, it’s not on the list of concerns.

Upsides of the Discover It Business card:

- Just as with the Discover It Miles personal card, the “Miles” (which are really points) are earned at a 1.5% rate for any purchase. The points earned at 1.5x in the first year (or 12 months), are matched (doubled) thus making it 3% card.

- The “Miles” earned are versatle: they can be redeemed for flights, travel or cashed out and sent to a linked bank account. Per Discover’s terms and conditions: “Starting at 1 Mile, you can redeem for cash as a electronic deposit to your bank account or for a credit for Travel Purchases on your statement made within in last 180 days. Travel Purchases include airline tickets, hotel rooms, car rentals, travel agents, online travel sites and commuter transportation. Redemption may not be available for approximately 24-48 hours if your card is reported lost or stolen.”

- Free cards for employees, although I don’t know if extra cards have a different account number or not

- The card’s spend likely isn’t reported monthly to credit bureaus, so if that’s the case, high spend/balances won’t affect credit utilization and your FICO score. However, I don’t know if this card will report mostly balances to credit bureaus.

- In my experience, there can be more leeway with higher spend on business cards than personal cards (in general)

- U.S. based customer service

Downsides to the Discover It Business:

- You’re allowed just 2 Discover credit cards at a single time. This seems to be a hard and set rule and includes business and personal card products.

- You need to have a Discover card open for a year before getting another card product

- Business credit card credit lines can’t be shifted to consumer credit cards (or vice versa), where two personal cards will have the ability to move/merge credit

- Cash back isn’t paid for an entire year. Those doing any non-organic (or manufactured spend) face a much longer wait time to get paid, and therefore have a greater chance of shutdown because of it)

- Payment hold times can be an issue

- Credit limit increases are done via a soft pull and can be done every 3 months for personal cards. I don’t know if this can happen with business cards.

- Product changes into personal cards may not be possible

- Credit lines could be more generous on business cards that with personal cards, which tend to be one the smaller side vs. other rewards cards

Conclusion

The main risk of applying for this card is the possibility of being approved for the card, but with a low credit limit. As I stated above, I’m not sure if credit limit increases multiple times a year is possible with business Discover cards (as it is with personal cards). If it’s not, that’s a significant aspect for people and/or businesses who are able to put large spend on cards. There’s a limited amount of credit cards offering greater than 2% cash back, and even with some question marks around it, this could be a great option for some with the right setup.